Unless otherwise noted, all trends below are for dollar sales within Nielsen U.S. off-premise channels for the one-week period ending 6/13/20 compared to the same week in 2019. We continue to remind our readers that we are only measuring some specific off premise channels, and that the impact of the health crisis on sales is uneven across companies in the alcohol industry.

Unless otherwise noted, all trends below are for dollar sales within Nielsen U.S. off-premise channels for the one-week period ending 6/13/20 compared to the same week in 2019. We continue to remind our readers that we are only measuring some specific off premise channels, and that the impact of the health crisis on sales is uneven across companies in the alcohol industry.

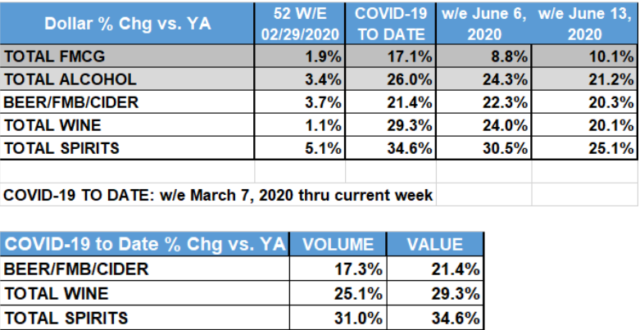

The year-over-year growth rate for total off-premise alcohol dollar sales within Nielsen measured channels is +21.2%.

- Spirits again led growth, +25.1% (down from +30.5% last week).

- Wine was +20.1% (down from +24% last week).

- Beer/FMB/cider growth is +20.3% (down from +22.3% last week). Beer specifically is +11.1%.

The following two graphics reflect the year-over-year change in dollar sales for the pre-COVID, ~full pandemic (15-week period ending 6/13/20) and recent one-week periods. The second graphic also includes year-over-year change in volume sales over the full pandemic period.

E-commerce

- During its peak in April, alcohol e-commerce sales levels were 6 times higher than comparable weeks of one year ago, primarily driven by increases in new buyers of alcohol online.

- Those increases in June to-date have now fallen to 3 times higher than a year ago, coinciding with a decrease in online alcohol buyers.

- Growth is still very impressive, but some consumers are likely returning to pre-COVID shopping patterns.

Consumer Insights

- Throughout COVID weeks, an increase in the number of households purchasing alcohol has been one of the primary drivers of growth for off-premise dollars.

- However, in recent weeks, the growth in the number of buyers is beginning to slow, up 14.7% for the 4 weeks ending 6/6/20 compared to those same 4 weeks last year.

- For a comparison, the number of buyers purchasing alcohol was up 16.2% for the 4 weeks ending 5/5/20, and up 20.5% for the 4 weeks ending 4/11/20 compared to last year.

- Throughout COVID weeks, liquor stores consistently have been driving much of the growth in buyers.

- The number of alcohol buyers in liquor stores is up 25.4% for the latest 4 weeks compared to last year.

- Grocery store alcohol buyers are up 14.2% compared to last year.

- Club buyers are also driving growth, up 17.2% compared to a year ago.

In the words of Danny Brager, Senior Vice President of Beverage Alcohol at Nielsen:

“As the on-premise space continues to expand openings across the country and we move from restricted living to re-opening, off-premise alcohol sales have experienced a steady slowing of growth since early May.

That said, we also have seen some recent and interesting trends in the growth of households purchasing items that correlate with celebrations, such as sparkling wine and higher-end wine and spirits. The timing of the spike in the number of households purchasing these celebratory items also coincides with Mother’s Day and college graduations.

All eyes will be on sales leading up to the upcoming July 4 holiday and long weekend, during a year unlike any other.”

In the words of Danelle Kosmal, Vice President of Beverage Alcohol at Nielsen:

“This was the first week since the beginning of March that beer/FMB/cider, with the significant tailwinds of hard seltzer, actually grew faster than wine.”

BEER/FMB/CIDER

Beer/FMB/cider dollar sales growth is +20.3%. Beer specifically is +11.1%.

- Growth rates for nearly all beer/FMB/cider segments are slowing compared to earlier COVID-19 weeks, except for super premiums and FMBs, which have maintained somewhat steady growth rates, up 22.7% and 19.0% respectively for the latest week.

- Hard seltzer growth rates continue to hover around 250% and maintain share above 10%, accounting for 10.4% of total category dollars for the latest week.

WINE

Wine dollar sales in Nielsen measured off-premise channels grew +20.1% in the most recent week vs. one year ago.

- The top 100 wine brands – accounting for approximately two-thirds of Nielsen measured off premise channel dollar sales – has seen some change since the beginning of March.

- Over these last 15 weeks, 4 brands entered the top 100 that were not there in the year prior – Castello del Poggio, Line 39, Rancho La Gloria, and Whitehaven.

- But in addition, several other brands – previously in the top 100 – moved up considerably higher within this top sales echelon. Brands that moved up 6 or more placements included (in alphabetical order): Bartenura, Bread & Butter, Cavit, Daily’s Cocktails, Decoy, Gerard Bertrand, Justin, Kim Crawford, Matua, Oliver, Risata, Stella Rosa (now in the top 10), Roscato, Starborough, and Whispering Angel.

- The brand diversity is remarkable – some non traditional wine types and packaging, strong NZ (Sauv Blancs), Italian, and California representation, an Indiana based winery, sweeter wines, and French rose’s.

Direct to Consumer Wine shipments for the month of May 2020 based upon Nielsen’s partnership with Wines Vines Analytics and Sovos ShipCompliant contained some other interesting insights.

- While wines made in the three western states and especially California account for the majority of overall DtC shipments, the highest shipment growth rates (over +50%) were from “remaining” USA – states beyond the big three wine producing states (CA, OR, WA).

- By winery size, the highest DtC shipment percentage growth rates were highly polarized, led by the largest wineries at one end (those over 500K cases annually) and the smallest ones at the other (limited production wineries under 1,000 cases annually), with growth for both segments over the last 3 months between +30% and +40% versus year ago. The latter group was much less likely though to make up for its on-site sales losses.

SPIRITS

Spirit sales in Nielsen measured off-premise channels grew +25.1%, the lowest level of growth since the week ending March 14, 2020, but still leading both wine and beer.

- While growth of most segments edged down just a bit, ready-to-drink (RTD) cocktails were an exception, as we’ve seen consistent growth rates over 80% for eleven consecutive weeks.

- Looking back over the last six weeks in aggregate, RTD cocktails sales are now bigger in Nielsen measured off-premise channels than both gin and Irish whiskey.

- After that, within the major spirit segments, Tequila remains comfortably in second place based on growth rates, followed by cordials, with cognac not too far behind.

- While whiskey growth was still double digits in the current week, its growth was over 10 percentage points less than last week’s growth.

Overview: Nielsen COVID-19 insights and analysis

- Nielsen.com: COVID-19: Tracking the Impact on FMCG, Retail and Media

- Nielsen.com: How Americans are Shopping During COVID-19

- Nielsen.com: Scenarios Beyond COVID-19: Rebound, Reboot, Reinvent

- Nielsen.com: Rebalancing the ‘COVID-19 Effect’ on Alcohol Sales

Nielsen CGA: COVID-19: Measuring the On Premise Impact